Half-Fare PLUS with SBB: when is it worth it?

by

@cycling_on_rails | RSS

This year, Switzerland’s SBB railways have introduced a new “Half-Fare PLUS” offer for regular travelers. The principle is simple: you deposit some money upfront and can receive a bonus to use within a year. For example, if you deposit 800 CHF, you obtain a bonus of 200 CHF, meaning that you have 1000 CHF to use within a year. If you don’t use everything when the plan expires, the bonus is lost but anything remaining from the initial deposit is refunded.

To make things more complicated, you can choose among three packages with various deposit amounts and bonuses.

| Age group | Deposit | Bonus | Total |

|---|---|---|---|

| Adult (25+) | 800 CHF | 200 CHF | 1000 CHF |

| Adult (25+) | 1500 CHF | 500 CHF | 2000 CHF |

| Adult (25+) | 2100 CHF | 900 CHF | 3000 CHF |

The pricing is also different between young travelers (from 6 to 24 years old) and adults (from 25 years old).

| Age group | Deposit | Bonus | Total |

|---|---|---|---|

| Young (6-24) | 600 CHF | 400 CHF | 1000 CHF |

| Young (6-24) | 1125 CHF | 875 CHF | 2000 CHF |

| Young (6-24) | 1575 CHF | 1425 CHF | 3000 CHF |

This new offer has sparked quite a few online discussions. When does it make sense to buy this offer? Which package should you choose? What are the pitfalls to avoid? Getting the most of it requires some analysis, which I detail in this article.

This post was last updated in 2024. If you’re reading this in a later year, chances are that the pricing has evolved due to inflation. In any case, information is provided here without guarantee, please refer to the official SBB website for official and up-to-date information.

Credit: SBB.

Credit: SBB.

A bit of math

Let’s start with an obvious case: if you’re sure to spend less than the minimal deposit within a year (800 CHF for adults, 600 for young people) there is no need to get the offer at all. If you may spend more than the bonus, getting the lowest “PLUS 1000” plan is a good option as you will be refunded up to the deposit amount if you end up spending less.

What is less clear is which of the three packages you should buy when you’re usual yearly spend is in between. The SBB website gives a few examples, but conveniently avoids the edge cases.

| Age group | Yearly spend (including half-fare) | Recommended deposit | Bonus |

|---|---|---|---|

| Adult (25+) | 3005.90 CHF | 2100 CHF | 900 CHF |

| Young (6-24) | 1416.40 CHF | 600 CHF | 400 CHF |

| Adult (25+) | 987.50 CHF | 800 CHF | 187.50 CHF |

| Adult (25+) | 1920 CHF | 1500 CHF | 420 CHF |

These examples are relatively clear. What is less clear is what to choose if for example you spend 1800 CHF a year as an adult. You may think that the second plan would be ideal as you would get 300 CHF of bonus on top of a 1500 CHF deposit, whereas the lower plan would only give you 200 CHF of bonus.

Yearly renewal of the Half-Fare PLUS 2000 plan.

Yearly renewal of the Half-Fare PLUS 2000 plan.

You can start any day of the year (in April in this example).

However, this simplistic calculation ignores an important fact: that you can renew the plan on a rolling basis before a full year if the credit has been fully used – as far as I understand the FAQ.

Can I “top up” my Half Fare Travelcard PLUS credit (before it expires)?

Once you have completely used up your customer deposit and are in the bonus phase, you can make another deposit for a new package and then receive the bonus that comes with it. The payment can be made at a staffed public transport point of sale or online at SBB.ch. The validity period is again one year from the selected first day of validity.

It is only possible to make a deposit for the same package size. If you would like a different package size, you will have to cancel your contract and conclude a new contract for the new package size.

Using the same scenario of a yearly spend of 1800 CHF – equivalent to 150 CHF per month – if you take the “PLUS 1000” plan, you would use the 1000 CHF credit within about 6 months and a half. For example, if you buy the PLUS 1000 plan in the beginning of January, you would finish it in the middle of July. You can (presumably) immediately buy another PLUS 1000 plan, which you would use until early February the following year.

Rolling renewal of the Half-Fare PLUS 1000 plan.

Rolling renewal of the Half-Fare PLUS 1000 plan.

If you continue like this indefinitely, you would get a 20% discount on a rolling basis, as you always pay 800 CHF of credit for the next 1000 CHF of purchases. This means that every year you get a bonus of 1800 * 20% = 360 CHF, which is higher than with the PLUS 2000 plan!

This strategy of starting with a smaller plan is also useful if you are not sure yet of how much you will spend in advance. If you end up spending only 1700 CHF, you would only get 1700 - 1500 = 200 CHF of bonus with the PLUS 2000 plan, but 1700 * 20% = 340 CHF with a renewed PLUS 1000 plan, a difference of 140 CHF!

Assuming that renewing the plan is allowed immediately upon expiry, the best way to compare the packages is in terms of how much discount they offer you once you fully spend them. The outcome is clear: even though in absolute terms the bonus for the PLUS 2000 plan looks more than twice larger than with the PLUS 1000 plan, in relative terms it’s only a difference of 5% once you spend more than 2000 CHF per year.

| Age group | Deposit | Total | Maximal discount |

|---|---|---|---|

| Adult (25+) | 800 CHF | 1000 CHF | -20% |

| Adult (25+) | 1500 CHF | 2000 CHF | -25% |

| Adult (25+) | 2100 CHF | 3000 CHF | -30% |

The relative difference between plans is even smaller for young travelers.

| Age group | Deposit | Total | Maximal discount |

|---|---|---|---|

| Young (6-24) | 600 CHF | 1000 CHF | -40% |

| Young (6-24) | 1125 CHF | 2000 CHF | -43.75% |

| Young (6-24) | 1575 CHF | 3000 CHF | -47.5% |

What does it change about GA?

Because of the high discount on the higher tiers (-30% or -47.5% depending on age), this new Half-Fare PLUS offer significantly shifts when it makes sense to get a GA Travelcard. As a reminder, the GA allows unlimited travel within almost all of Switzerland (detailed area of validity), for the following yearly1 pricing at the time of writing.

| Age group | Yearly GA (2nd class) | Yearly GA (1st class) |

|---|---|---|

| Child (6-15) | 1720 CHF | 2850 CHF |

| Young (16-24) | 2780 CHF | 4450 CHF |

| Twenty-five (25) | 3495 CHF | 5670 CHF |

| Adult (26+) | 3995 CHF | 6520 CHF |

Before the Half-Fare PLUS, the break-even point was simple: you should get a GA if the sum of a Half-Fare Travelcard plus all your half-fare tickets exceeded the yearly price of the GA. With the Half-Fare PLUS, you can travel more than that without reaching the yearly GA rate, thanks to the higher discounts on the PLUS 3000 plan.

To help decide between a GA and the Half-Fare PLUS package(s), I’ve calculated the break-even points and summarized them in the following table, depending on the age group and train class. You can also find the same information in charts just below.

| Age group | Class | Half-Fare Travelcard | Old break-even point | New break-even point |

|---|---|---|---|---|

| Child (6-15) | 2nd | 0 CHF | 1720 CHF | 3276.19 CHF |

| Young (16-24) | 2nd | 100 CHF | 2680 CHF | 5104.76 CHF |

| Twenty-five (25) | 2nd | 170 CHF | 3325 CHF | 4750 CHF |

| Adult (26+) | 2nd | 170 CHF | 3825 CHF | 5464.29 CHF |

| Child (6-15) | 1st | 0 CHF | 2850 CHF | 5428.57 CHF |

| Young (16-24) | 1st | 100 CHF | 4350 CHF | 8285.71 CHF |

| Twenty-five (25) | 1st | 170 CHF | 5500 CHF | 7857.14 CHF |

| Adult (26+) | 1st | 170 CHF | 6350 CHF | 9071.43 CHF |

Notable exceptions

There is however an important caveat: the Half-Fare PLUS cannot be used to purchase travelcards. If you are spending thousands per year on public transport, chances are that a point-to-point or regional travelcard is cheaper for you than individual tickets (if you always commute on a given route), and you cannot pay for that with the Half-Fare PLUS.

To give a concrete example, a single ticket between Zurich and Bern costs 26.5 CHF so a daily commute 200 days per year would cost 10600 CHF, well above the break-even point for the GA.

Another case: a single ticket between Aarau and Zurich costs 13.4 CHF so traveling 200 days per year would cost 5360 CHF, i.e. 3752 CHF after the -30% discount that you can get with Half-Fare PLUS 3000. This is slightly below the GA break-even point, but an annual point-to-point ticket for this specific route costs only 3192 CHF.

In short: you should do the math based on your specific needs to know which plan would be the most beneficial.

Another important exception is that you cannot use your Half-Fare PLUS credit to pay for RailAway offers, which combine a train ticket with various excursions (museums, ski resorts under the “Snow’n’Rail” branding, etc.) at a discount – 10% to 50% depending on the destination.

Likewise, international tickets cannot be bought with Half-Fare PLUS credit. The complete list of compatible and incompatible tickets is available in the FAQ.

Practical caveats

Now that I’ve covered the financial theory, there are some practical aspects to mention about the Half-Fare PLUS plan.

The first one that surprised me is that you cannot buy the plan and start using it on the same day, the first day of validity of the plan has to be at least one day later. This is explained in the contractual conditions (German) and summarized in the FAQ. I got bitten by this as I was planning a big day trip but realized too late that I couldn’t benefit from the bonus on that trip.

The second part was that the payment system didn’t work on the day I finally purchased the package. I tried various online options, but kept getting an error.

The payment error I’ve faced when trying to credit my Half-Fare PLUS plan.

The payment error I’ve faced when trying to credit my Half-Fare PLUS plan.

The Half-Fare PLUS payment method cannot be used until the credit is paid.

The Half-Fare PLUS payment method cannot be used until the credit is paid.

So I ended up having to go to the counter the next day, with a waiting time of one hour in Zurich’s main station! I lost another day of the plan because of that, as once the contract was concluded I couldn’t shift the date but also couldn’t use it until I topped up the money… Quite an annoying experience, but fortunately my friends could pay normally on other days, so I hope you don’t get any technical issues.

There are also important caveats related to renewal. Even though I haven’t reached them yet, a careful reading of the conditions reveals the following.

First of all, the plan is automatically renewed after one year. If you don’t want to have another large bill to pay upfront next year, be prepared to cancel in advance!

Second, upgrading or downgrading to a different plan requires canceling the contract first (which means losing any remaining bonus), and then making a new contract with the new plan. A bit of friction where you may lose a bit of the bonus if you’re not careful in the transition period.

Lastly, something that is less clear is what happens when you get close to the end of the bonus, in particular if you want to pay a ticket that costs more than your remaining bonus. Normally, you can select “Half-Fare PLUS” as a payment method in the SBB app, but it’s unclear if the app allows splitting a payment between several methods – remaining bonus plus a credit card for example. The FAQ explains that you can top up your credit by purchasing a new package once you are in the bonus phase, so that may not be a problem if you intend to renew anyway (to be confirmed once I end up renewing my plan). Otherwise, it might be that you lose a bit of bonus if you intend to cancel your plan.

Don’t hold your breath though: according to this forum discussion, renewal wasn’t possible in March 2024, presumably due to technical issues. An article published in the Tages Anzeiger on the 19th of March 2024 concurred with renewal being impossible at that time.

Conclusion

Even though the Half-Fare PLUS offer description is relatively simple – pay upfront and get a bonus on top of that – in reality getting the most of it requires financial planning. In principle this offer can bring up to 30% discount for adults, but in reality most passengers won’t get to it: regular commuters will likely benefit from a point-to-point travelcard while leisure travelers may use a RailAway offer, none of which are compatible with the Half-Fare PLUS.

Another effect is that anyone getting close to the start of their bonus may be driven to spend more than they would have to “benefit” from the bonus, a psychological bias that loyalty schemes commonly leverage to boost revenue.

Other reasons for criticism: the offer is only available for passengers using the app – as reported by a consumer protection association – increasing the impact of the digital divide. There is also a question of fairness, as those spending more get a proportionally better discount: someone spending 500 CHF per year gets no benefit from the offer, whereas someone spending 5000 CHF per year gets a whole 30% off. In particular, first class travelers are more likely to reach the higher tiers than their second class counterparts.

Meanwhile, SBB has discontinued the Leisure Travelcard (archive) as of 31 March 2024, another package that was offering 20 or 30 day cards to use within a year at a much more attractive price2. Together with the average ticket increase of around 4% in 20243, it’s clear that SBB is tightening its finances.

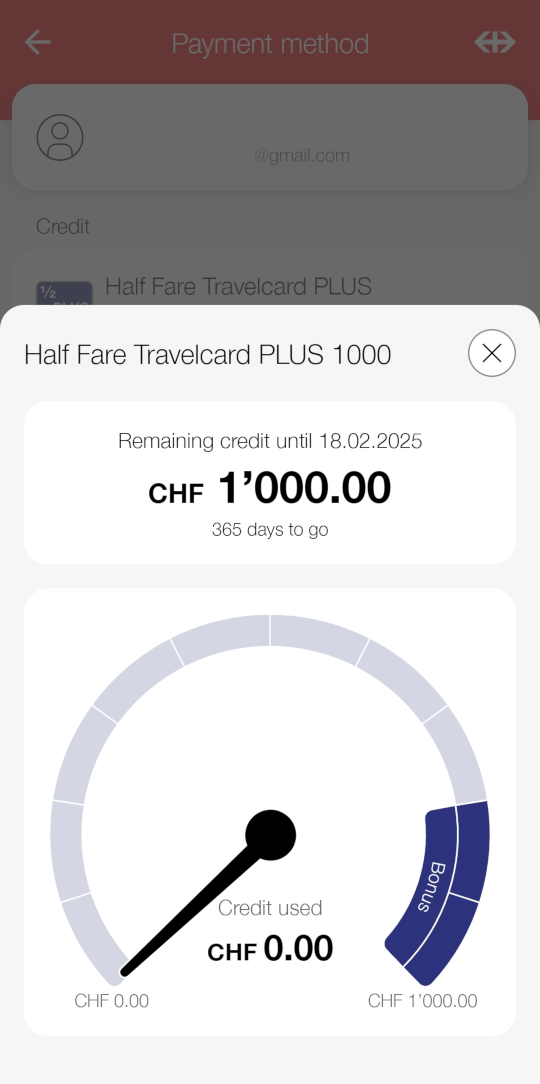

Personally, I took the Half-Fare PLUS 1000 as I mostly travel for leisure. One thing I like is that it’s easy to track how much I’m spending over time directly in the SBB app.

Ready to roll!

Ready to roll!

I will update this post when I reach the renewal phase.

-

Monthly pricing of the GA is also available for periods of 6 months minimum, and is 4% to 15% more expensive than the yearly rate depending on age and tier (second or first class). ↩

-

20 days were generally offered for 900 CHF, with occasional offers for 620 CHF, instead of 20 * 75 CHF = 1500 CHF, that is a discount of -40% to -59%. ↩

-

According to a note of the Swiss Pass Alliance available in German, French and Italian. ↩

Comments

To react to this blog post please check the Mastodon thread.

You may also like